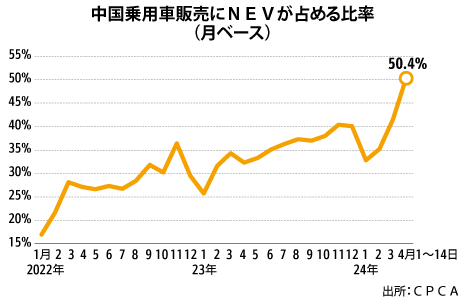

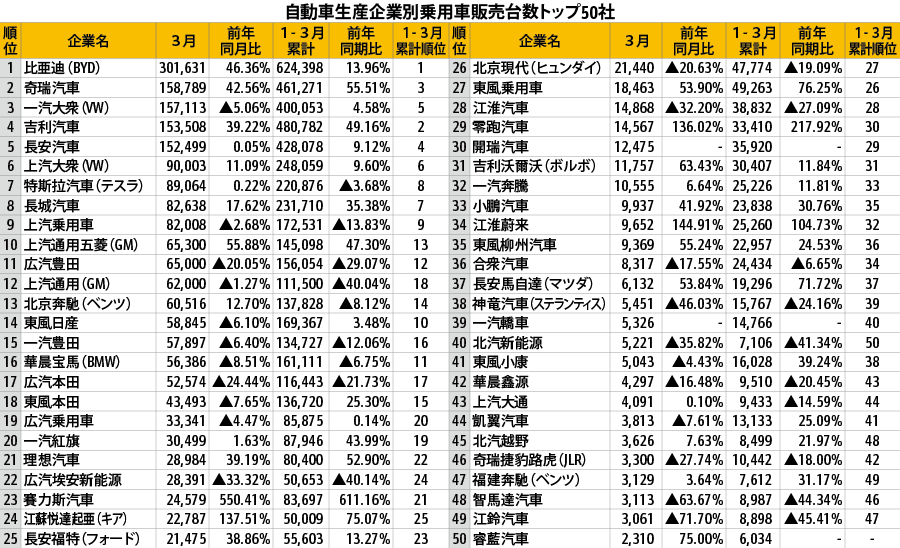

中国乗用車の新エネ車率5割超え内燃機関車が少数派の時代到来PICK UP車両自動車統計政策・法律・規制中国の自動車業界団体によると、4月1~14日に販売された乗用車に新エネルギー車(NEV)が占める比率は50%を超えた。統計対象の期間を問わず、NEVの比率…

シンガポール早ければ年内に最初の認可ウマミの培養肉商業化計画(上)独自PICK UP食品食品・飲料バイオベンチャー希少で養殖が難しい魚類の培養肉の開発を手がけるシンガポールのウマミ・バイオワークス(旧ウマミ・ミーツ)が、国内での製品販売に向けて規制当局の認可取得に…

フィリピンペソ安進行、約1年半ぶり1ドル57ペソ台、米利下げ遅れで独自PICK UP金融金融一般証券マクロ経済政策・法律・規制フィリピンペソが対米ドルで下落している。19日の為替市場では1米ドル=57.650ペソと7日続落した。2022年11月10日以来、約1年6カ月ぶりの安値となった。米国…

タイ米中対立で増すタイの重要性電子部品デルタ現法トップに聞く独自PICK UPIT電子・コンピューター台湾の台達電子工業(デルタ)はタイで電気・熱制御関連の商品の製造から事業を開始し、現在はパワーエレクトロニクス、自動化システム、インフラ、モビリティー…

韓国大統領府秘書室長に与党重鎮、国政刷新アピール政治政治一般選挙外交【ソウル共同】韓国の尹錫悦(ユンソンニョル)大統領は22日、大統領府秘書室長に与党「国民の力」の重鎮で韓日議員連盟会長の鄭鎮碩(チョンジンソク)氏を充て…

タイ中国EVの供給網構築(下)独自PICK UP車両自動車環境政策・法律・規制車部品タイの電気自動車(EV)市場の拡大は、日系の自動車部品メーカーにとって新たな商機となる。昨年に存在感が一気に拡大したことから、中国系完成車メーカーに関……

タイアセアンでの事業拡大目指すPICK UP金融金融一般今年2月に2026年までの第4次中期経営計画を発表したタイのアユタヤ銀行。日本企業の投資をタイに呼び込んだり、タイ企業の海外進出を後押ししたりする上で、東……

シンガポール同業と合併で事業範囲を拡大独自PICK UP食品食品・飲料バイオ希少で養殖が難しい魚類の培養肉の開発を手がけるシンガポールのウマミ・バイオワークスは、同業で甲殻類の培養肉開発を専門とするシオック・ミーツとの合併を進……