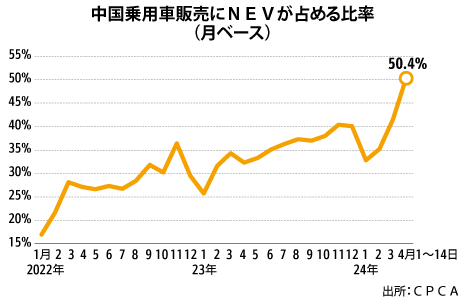

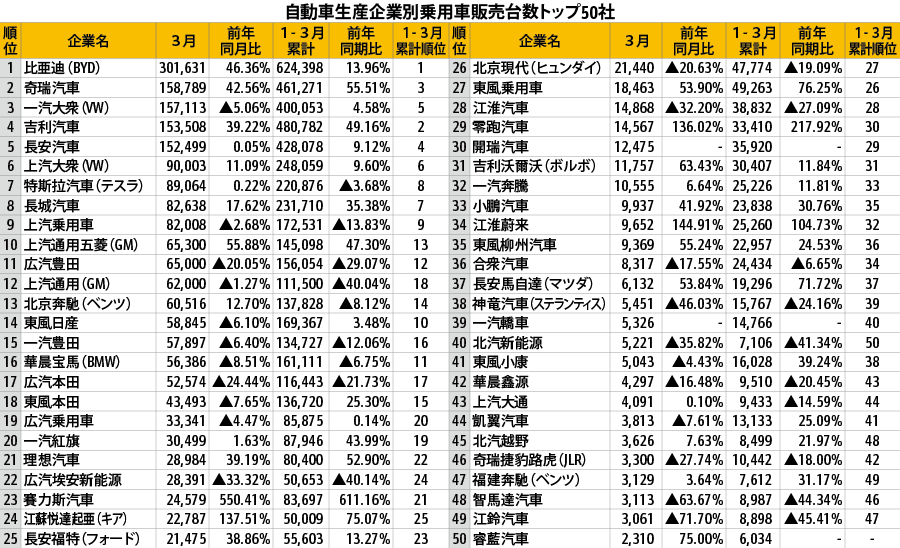

中国乗用車の新エネ車率5割超え内燃機関車が少数派の時代到来PICK UP車両自動車統計政策・法律・規制中国の自動車業界団体によると、4月1~14日に販売された乗用車に新エネルギー車(NEV)が占める比率は50%を超えた。統計対象の期間を問わず、NEVの比率…

タイタイの脱炭素での貢献目指すアユタヤ銀大和頭取に聞く<上>PICK UP金融金融一般2013年に三菱UFJファイナンシャル・グループの傘下に入ったタイのアユタヤ銀行。今年2月には第4次となる中期経営計画を発表し、26年までに「To be the Lead…

ミャンマータイ国境緊迫、警戒と支援避難民3千人、流入抑制措置もPICK UP政治政治一般外交軍事文化・宗教タイが、ミャンマーからの避難民流入に警戒感を強めている。両国の主要玄関口付近で武力衝突が激化し、緊迫する状況がより深刻化すれば避難民の大量流入も起こり…

ベトナム東京海上、地場企業開拓へ物流分野で提携、リテールも視野独自PICK UP金融保険東京海上グループのベトナム法人、東京海上ベトナムが地場企業向けの損害保険事業を拡大している。3月末には地場宅配・物流大手ノイバイ・エクスプレス・アンド…

韓国大統領府秘書室長に与党重鎮、国政刷新アピール政治政治一般選挙外交【ソウル共同】韓国の尹錫悦(ユンソンニョル)大統領は22日、大統領府秘書室長に与党「国民の力」の重鎮で韓日議員連盟会長の鄭鎮碩(チョンジンソク)氏を充て…

タイ中国EVの供給網構築(下)独自PICK UP車両自動車環境政策・法律・規制車部品タイの電気自動車(EV)市場の拡大は、日系の自動車部品メーカーにとって新たな商機となる。昨年に存在感が一気に拡大したことから、中国系完成車メーカーに関……

タイアセアンでの事業拡大目指すPICK UP金融金融一般今年2月に2026年までの第4次中期経営計画を発表したタイのアユタヤ銀行。日本企業の投資をタイに呼び込んだり、タイ企業の海外進出を後押ししたりする上で、東……

シンガポール同業と合併で事業範囲を拡大独自PICK UP食品食品・飲料バイオ希少で養殖が難しい魚類の培養肉の開発を手がけるシンガポールのウマミ・バイオワークスは、同業で甲殻類の培養肉開発を専門とするシオック・ミーツとの合併を進……