タイ中国EVの供給網構築(上)地場から調達、国産化規制に対応車両自動車車部品政策・法律・規制環境NEWタイは今年、中国系メーカーによる電気自動車(EV)生産の元年を迎えた。タイ政府が優遇措置で国産化の要件を定めていることなどを背景に、EVのサプライチェ…

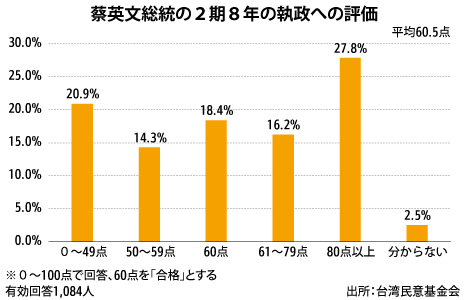

台湾蔡総統への評価、平均60.5点世論調査、8年の執政「合格点」PICK UP政治統計政治一般選挙NEW台湾の民間シンクタンク、台湾民意基金会が23日に発表した世論調査によると、蔡英文総統の2期8年にわたる執政への評価(0~100点で回答、60点を「合格」とする…

マレーシアサラワクが化合物半導体製造英機関と覚書、まず英拠点設置へPICK UPITIT一般電子・コンピューターNEW東マレーシア・サラワク州政府傘下でテクノロジー関連の調査や開発を手がけるSMDセミコンダクターは23日、英ロンドンで英政府機関の化合物半導体応用(CSA…

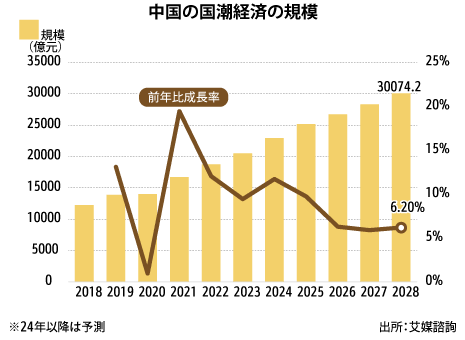

中国中国ブランド推しが拡大へ市場規模は28年に3兆元超えPICK UP経済自動車電機その他製造小売りマクロ経済統計NEW中国で数年前から顕在化している「国潮」(中国ブランドの商品を評価する機運)が今後ますます強まる見通しだ。中国市場調査会社の艾媒諮詢(IIメディアリサー…

韓国大統領府秘書室長に与党重鎮、国政刷新アピール政治政治一般選挙外交【ソウル共同】韓国の尹錫悦(ユンソンニョル)大統領は22日、大統領府秘書室長に与党「国民の力」の重鎮で韓日議員連盟会長の鄭鎮碩(チョンジンソク)氏を充て…

タイ中国EVの供給網構築(上)車両自動車環境政策・法律・規制車部品NEWタイは今年、中国系メーカーによる電気自動車(EV)生産の元年を迎えた。タイ政府が優遇措置で国産化の要件を定めていることなどを背景に、EVのサプライチェ……

タイアセアンでの事業拡大目指すPICK UP金融金融一般今年2月に2026年までの第4次中期経営計画を発表したタイのアユタヤ銀行。日本企業の投資をタイに呼び込んだり、タイ企業の海外進出を後押ししたりする上で、東……

シンガポール同業と合併で事業範囲を拡大独自PICK UP食品食品・飲料バイオ希少で養殖が難しい魚類の培養肉の開発を手がけるシンガポールのウマミ・バイオワークスは、同業で甲殻類の培養肉開発を専門とするシオック・ミーツとの合併を進……

タイ【タイ会計・税務解説】第1回 新規赴任者のためのタイ会計税務(1)経済マクロ経済政策・法律・規制NEWタイに新規赴任された方々を対象にタイでの会計税務の基礎的な部分を2回にわたり解説致します。今後タイにおける会計税務の各論点について当記事内にて詳細に解説……

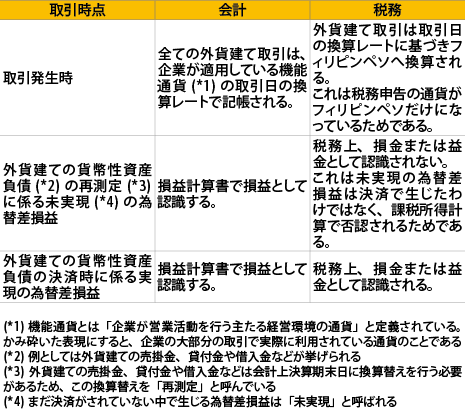

フィリピン【役立つ税務】第54回 外貨建て取引に係る問題経済マクロ経済金融一般政策・法律・規制財政NEW■はじめに フィリピン内国歳入庁(BIR)が2024年1月22日に通達「RMC No.12-2024」を公表し、外貨建て取引から生じる為替差損益に係る会計上と税務上の取り……