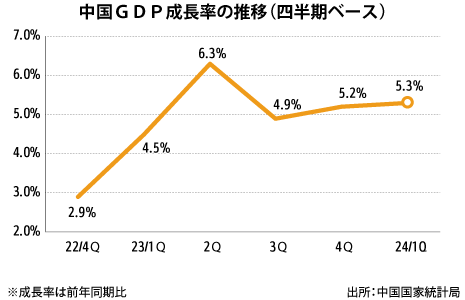

中国1~3月の成長率は5.3%前期から拡大も先行きに不安残すPICK UP経済自動車その他製造マクロ経済統計貿易政策・法律・規制インフラ設備投資雇用・労務NEW中国国家統計局は16日、2024年第1四半期(1~3月)の実質国内総生産(GDP、速報値)成長率が前年同期比5.3%だったと発表した。成長率は23年第4四半期(1…

フィリピン電力逼迫、ルソン島に警報1年ぶり、発電所20カ所停止PICK UP公益電力・ガス・水道マクロ経済政策・法律・規制インフラNEWフィリピン全国送電社(NGCP)は16日、マニラ首都圏がある北部ルソン島で電力需給の逼迫(ひっぱく)レベルが最も深刻なことを示す警報「レッドアラート」を…

タイ県知事、「信頼回復」に全力チェンマイ大気汚染改善へ(下)独自PICK UP社会保健医療農林・水産観光政策・法律・規制社会一般NEW観光業が収入の大半を占めるタイ北部チェンマイ県にとって、大気汚染のイメージ払拭と観光客からの信頼回復は最重要課題だ。2022年10月に就任したニラット県知事…

インドネシア動き出すスバン県の工業団地西ジャワ新経済地域を創生(2)独自PICK UP経済陸運海運マクロ経済貿易政策・法律・規制インフラNEWインドネシア西ジャワ州スバン県が、次世代の成長地域として注目されつつある。同県は日系企業が集積する工業地帯がある同州カラワン県に隣接し、2021年12月にパ…

韓国ネット銀の新規認可、野党圧勝で推進に速度PICK UP経済マクロ経済IT一般通信金融一般政治一般政策・法律・規制選挙小売り韓国でこのほど実施された総選挙で革新系野党「共に民主党」が圧勝したことを受け、同党が公約として掲げたインターネット専業銀行の新規認可や通信端末の価格引…

シンガポール【アジアで会う】嶋野圭介さん 千葉銀行シンガポール駐在員事務所長社会金融一般社会一般しまの・けいすけ 1980年千葉市生まれ。県立千葉高校から千葉大学法政経学部に進み、新卒で2004年に千葉銀行に入行という「千葉づくし」の経歴を持つ。中学生の……

韓国【24年総選挙】「尹氏の政治姿勢に憤り」独自PICK UP政治政治一般軍事選挙外交韓国総選挙は与党「国民の力」が選挙前の議席も割り込む大敗を喫した。一方、最大野党「共に民主党」は協力する曺国(チョ・グク)氏の新党「祖国革新党」と合わ……

タイ観光に打撃続き、健康懸念も独自PICK UP社会保健医療農林・水産観光社会一般政策・法律・規制タイ北部の観光都市チェンマイの大気汚染が今年も深刻だ。県政府によると、微小粒子状物質「PM2.5」の濃度は前年比で大幅に低下したが、依然として安全基準値を……

オーストラリア【オーストラリアビジネスのからくり】第112回経済マクロ経済政策・法律・規制オーストラリアの雇用関係の法務には、まことしやかな言い伝えがあります。本コラム3月分で3点取り上げたところです。今回のその続き2点となります。 ◇(4)……

シンガポール【RHQの真価と進化】アジア市場への強みの伝承経済マクロ経済外食・飲食第10回 前回はコーポレート部門強化の中で、組織構造や制度面からアジア事業の中長期のポテンシャルをいかに最大化するかについて論じた。今回は題材を変え、アジ……